Assessing the options when exiting Clerical Medical Group Pension Contracts

The recent announcement by Clerical Medical outlining their intention to exit the Defined Benefit pension market by June 2028 (at the latest) is forcing trustees and sponsors using their services to consider alternatives.

As an independent professional trustee to several Group Pension Contract (GPC) schemes over many years, Vidett have already successfully exited the GPC contract on a selection of schemes in recent years prior to Clerical Medical’s announcement.

Given this experience, we’re well placed to guide trustees and sponsors through the various options available. Whilst the recent communication from Clerical Medical suggests trustees and sponsors only have three options. We see four, depending on a scheme’s circumstances:

Different schemes, different governance needs

Data from the Pension Protection Fund’s Purple Book 2025 shows why a single governance framework is now unrealistic. Around 80% of schemes have fewer than 1,000 members, but these account for a small share of assets. By contrast, a small number of large schemes hold most DB assets and membership. This creates two governance worlds:

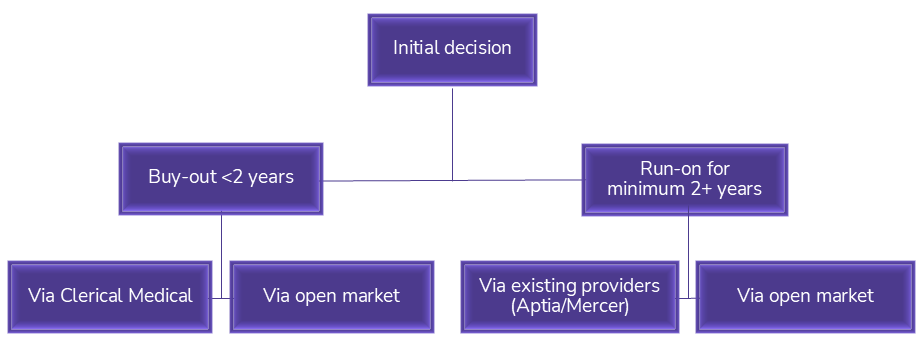

The initial decision

Does the sponsoring employer have the financial resources and desire to fund the scheme to a short-term buy-out (within 2 years)? If yes, trustees could consider a buy-out. If not, running on for at least another 2 years will be the default position. But even within these two options there are choices to make…

Buying-out with Clerical Medical

Some schemes will find it sensible to stay with their existing provider as Clerical Medical are guaranteeing to offer buy-out terms for all schemes, irrespective of size. However, with Clerical Medical exiting the market there are considerations.

Most importantly, you need to be confident the project can complete before the June 2028 deadline, including the completion of Guaranteed Minimum Pension equalisation (GMPe) (where required), as the approach with Clerical Medical is straight to buy-out rather than buy-in followed by buy-out.

Speaking of GMPe, Mercer and Aptia will continue to provide actuarial and administration services when schemes stay. The cost here will continue to be covered under the GPC terms (expected to be 1.4% of invested assets during 2026), This will suit schemes with a low level of invested assets better than larger ones. The costs for completing GMP equalisation and the work associated with winding-up the scheme will need to be agreed with Mercer/Aptia.

Staying with Clerical Medical means the invested assets (not insured annuities) will remain in their with-profits fund, meaning they won’t move in line with the scheme’s liabilities. Any difference between the current asset value and the buy-out cost will fluctuate. Schemes will not receive an enhanced surrender value but will continue to benefit from the Guaranteed Annuity Rates under the GPC, including upon eventual buy-out. An annual charge of circa 0.875% of the invested assets is made to subsidise the cost of providing the guarantees.

Buy-out on the open market

Some trustees will assess the above and decide that buy-out elsewhere is more suitable. There’s no requirement with other providers to complete the project by June 2028, offering more leniency if timelines slip. Schemes will benefit from an enhanced surrender value but lose access to the Guaranteed Annuity Rates. Notably, for the cases that we have reviewed, the enhanced surrender value has been higher than the estimated value of the Guaranteed Annuity Rates. Following the surrender of assets, they can be invested in a way that helps to hedge against the movement in the scheme’s liabilities (providing more certainty over the cost to buy-out).

Schemes moving away from Clerical Medical will need to source actuarial, administration and investment consultancy services from the open market (which may cost more than the charges levied under the GPC, particularly for schemes with a low level of invested assets, and administration services will need to include treasury management for running a trustee bank account, pensioner payroll for any new retirements (pre buy-out) and GMPe. Connecting or maintaining connection to Pension Dashboards will need to be considered for relevant schemes as well.

However, there are opportunities, for example: you will have control over the firm appointed and can negotiate service level agreements; the onboarding can be tailored to ensure GMP data is cleansed and ready for going to the buy-out market in the short term. Schemes will of course have a choice of buy-out provider, but not all bulk annuity providers will be willing to quote, especially for small schemes.

Preparing for run on

If running a scheme on looks a more suitable initial decision, then there is a new set of factors to consider. Schemes will again see the enhanced surrender value while losing access to Guaranteed Annuity Rates, while assets can be invested to hedge against movement in the scheme’s liabilities.

But this is balanced against the need for new services including investment consultancy, treasury management services for running a trustee bank account and pensioner payroll. The fees for these as well as any foreseeable project work (completing GMP equalisation, dashboard connection, data cleansing etc) will need to be weighed up.

Run on with Aptia/Mercer or new providers

You should assess your experience of service standards under Mercer and Aptia, as well as the cost of remaining with them or moving. When looking at moving, initial ‘take-on’ fees should be accounted for.

Transferring administration services to a new provider can be challenging, but it can also be a good way of drawing out any data and/or benefit issues and giving the scheme a ‘clean start.’ Meanwhile, if you do decide to move away from Aptia/Mercer then it’s better to avoid moving actuarial services ‘mid-triennial valuation’ as it’s quite likely that assumptions will change upon exiting the GPC.

You shouldn’t feel wedded to Mercer/Aptia either, as other advisers have developed tailored solutions for extraction from GPC arrangements. Additionally, the small schemes ongoing proposition that some consultancies have developed could be a good fit for some.

Other factors

Regardless of the option you choose, we’ve found scheme documentation (including policy details) is often missing or incomplete and so it is beneficial to work with legal advisers who have experience of these arrangements, including extraction from the GPC (where relevant). Any additional voluntary contributions (AVCs) held with Clerical Medical will need to find a new home as they won’t assign these into members own names. Finally, for schemes in GPCs that purchase pension increases on an annual basis, arrangements will need to be made to secure future increases, especially where existing pensioners remain with Clerical Medical and deferred members are transferred to a new provider.

Whilst schemes must exit their GPCs by July 2028, there are multiple ways to do so. To achieve the best possible outcomes for members, it’s important to consider what option is right for your scheme.

If you’d like to learn more, why not talk to Chris or learn how he helped a client exit an insured arrangement.